Operating 1.7 million chargers already in the UK

For years, EV charging has often been discussed through one dominant question: are enough chargers being installed?

That question still matters, but it no longer captures the full strategic importance of the sector. Charging infrastructure is now becoming one of the foundations of the wider EV economy. It connects mobility, energy, real estate, grid capacity, software, consumer behaviour and industrial policy.

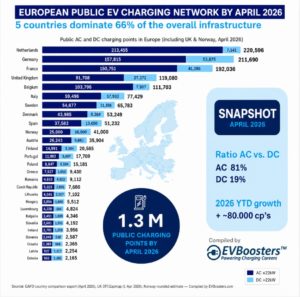

The report shows that the UK has already rolled out more than 1.7 million chargers across homes, businesses and the public network, including more than 120,000 public chargers. The public charging network has doubled in size over the last three years, showing how quickly the market has moved from early adoption to large scale infrastructure development.

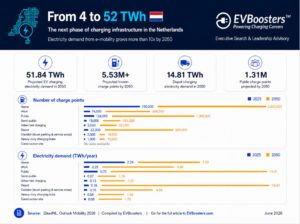

The next phase will be larger, more complex and more capital intensive. By 2035, the UK public charging network is projected to grow to more than 500,000 charge points, while total EV charging electricity demand could reach 43 TWh. Public charging will become increasingly important as more drivers without access to home charging enter the EV market.

This changes the strategic role of charging. It is no longer only about placing hardware in the ground. It is about enabling consumer confidence, fleet electrification, clean transport, energy flexibility and future industrial competitiveness.

The economics are beginning to shift

The report also highlights a critical reality. The sector is still investing ahead of demand.

Despite a current revenue base of around £2.5 billion, direct economic value added remains relatively low because companies are still deploying significant capital into infrastructure before utilisation and profitability fully mature. In other words, the sector is building now in order to support the market that will arrive later.

That is typical for infrastructure markets in their buildout phase. The economics improve when utilisation rises, operational efficiency increases and platforms benefit from scale. LCP Delta expects the sector to reach £2.5 billion in annual direct GVA by 2035, with direct employment growing from around 12,000 today to 36,000 jobs.

These are not only installation jobs. They include roles across charge point operation, software, engineering, manufacturing, energy retail, flexibility services, customer operations, finance, sales and data. As the sector matures, the organisational complexity behind the charging network will increase significantly.

The investment requirement is equally significant. The sector could attract £30 billion in external investment by 2035, provided policy remains predictable, EV adoption continues and operators move towards sustainable margins.

Policy confidence remains essential

The report is clear that this growth is not automatic. The UK’s ZEV Mandate plays a central role in creating long term demand visibility. Investors, CPOs, manufacturers, installers, software providers and energy companies all need confidence that EV adoption will continue at scale.

If policy becomes unpredictable, investment slows. If investment slows, infrastructure availability weakens. If infrastructure availability weakens, consumer confidence suffers.

The UK therefore faces a strategic choice. It can treat EV charging as a cost attached to the energy transition, or it can treat it as a growth platform for industrial development, skilled employment, infrastructure investment and energy resilience.

Execution will separate the winners from the rest

The next decade will not only be defined by capital availability or charger deployment targets. It will be defined by execution quality.

The sector is moving from early market expansion into a more mature infrastructure phase. That transition creates new organisational demands. Companies will need to manage larger asset bases, improve utilisation, strengthen uptime, professionalise commercial operations, build deeper partnerships with grid operators and landlords, and create more disciplined capital allocation models.

This requires a different leadership profile from the one that was sufficient in the first phase of the market. Entrepreneurial speed remains important, but it now needs to be combined with operational rigour, financial discipline, stakeholder management and the ability to scale organisations without losing focus.

For many companies, this will be a difficult transition. The skills needed to raise capital, enter a market and win early contracts are not always the same skills required to operate critical infrastructure at scale. The next phase will demand leadership teams that can combine growth ambition with reliability, commercial focus with stakeholder alignment, and innovation with operational discipline.

From first movers to long term infrastructure platforms

The winners will not simply be the companies with the largest number of chargers. They will be the companies that can finance, deploy, operate and optimise charging infrastructure as critical infrastructure.

That has implications for boards, investors and leadership teams across the sector. Leadership quality will become an increasingly important value driver. Founders will need to assess when the organisation around them must evolve. Boards will need to understand whether current management teams are ready for the next phase. Investors will look more closely at whether companies can convert market growth into scalable, profitable and resilient operations.

At EVBoosters, this is where we see the market changing across Europe. EV charging companies are moving from scale up to infrastructure platform, from local expansion to international execution and from founder led energy to professional leadership teams.

The companies that build the right leadership teams now will be better positioned to attract capital, execute at scale and turn charging infrastructure into long term strategic value.

The £385 billion opportunity is therefore not only an economic opportunity. It is a leadership challenge. And the companies that understand this early will be the ones most likely to shape the next decade of e Mobility.