Market composition versus size and focus on growth numbers

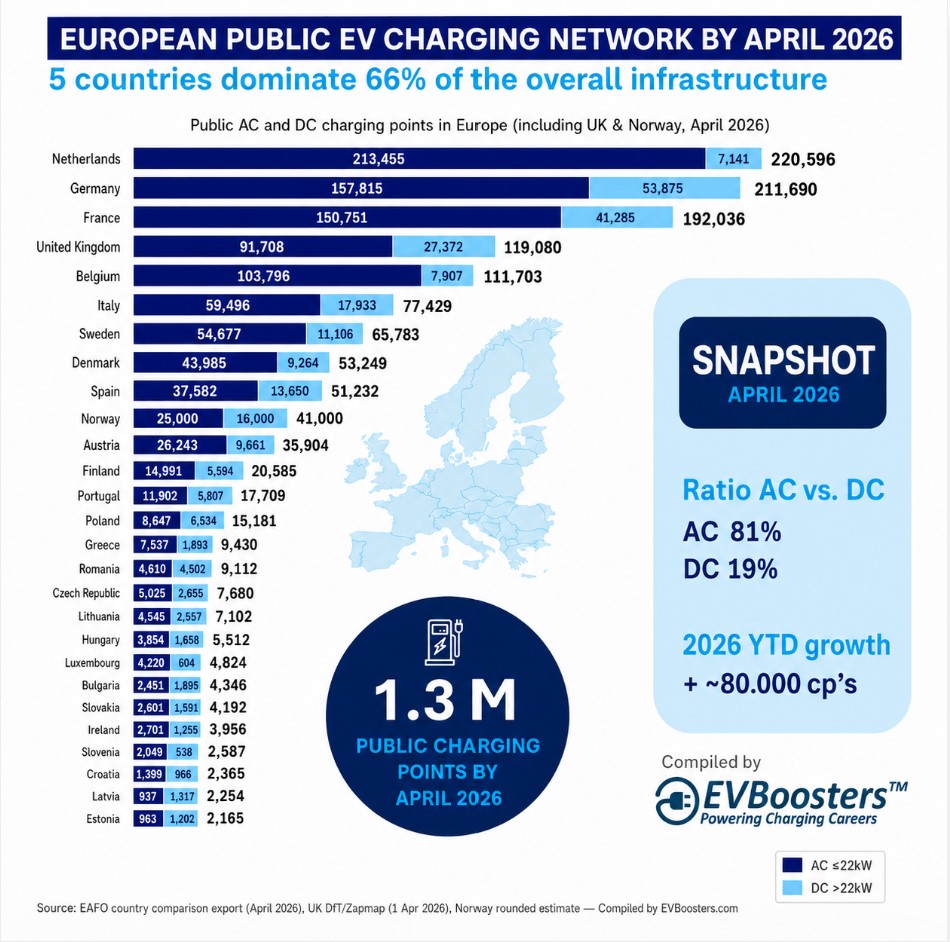

Across the EU27, EAFO reports 927,024 public AC charging points and 212,439 public DC fast chargers in April 2026. That means the European public charging network is still roughly 81% AC and 19% DC.

This reflects how the market has developed over the past decade. AC charging remains the backbone of public charging in many countries, especially in cities, residential neighbourhoods, public parking, workplace locations and destination charging environments.

But the country differences are becoming more important. The Netherlands and Belgium are strongly AC led markets. Germany, France, the United Kingdom, Italy and Spain have a much higher DC share. Their networks are more balanced between local public charging and faster charging for longer trips and higher usage cases.

This shows why total charge point numbers alone are no longer enough to assess market maturity. The composition of the network now matters just as much as its size.

Europe added around 78,000 public charge points in early 2026

The EAFO infrastructure export shows that the EU27 public charging network grew from 1,061,890 public AC and DC charging points at the end of 2025 to 1,139,463 by April 2026.

That represents an increase of 77,573 public charging points in the first months of 2026.

Most of that growth still came from AC infrastructure. The EU27 added 59,890 AC charging points and 17,683 DC charging points between the end of 2025 and April 2026.

This confirms that the European rollout is still moving at pace. But it also shows that the discussion is shifting. The central question is no longer only whether Europe is installing enough charging points. It is whether the right type of infrastructure is being deployed in the right locations.

Germany has almost eight times more DC chargers than the Netherlands

The biggest insight from the April 2026 data is not the total number of charging points. It is the difference between AC and DC infrastructure. The Netherlands has built a very dense public charging network, but it is overwhelmingly AC based. EAFO reports 213,455 AC charging points in the Netherlands, compared with only 7,141 DC charging points.

Germany has fewer total public charging points than the Netherlands, but a much stronger fast charging base. It operates 157,815 AC charging points and 53,875 DC charging points. That means Germany has 7.5 times more public DC chargers than the Netherlands. Rounded for market interpretation, Germany now has almost eight times more DC charging infrastructure, despite the Netherlands still leading in total public charge points.

This distinction matters. A high number of AC charging points supports local density, everyday charging and urban accessibility. A strong DC network supports long-distance travel, motorway corridors, high-mileage drivers, taxis, commercial fleets, and logistics electrification.

The next phase will be about quality, not only quantity

Europe has built a large public charging base. Reaching around 1.3 million public charging points is a significant milestone. But the April 2026 data makes clear that the next phase will be more complex.

The Netherlands shows the strength of a dense AC network. Germany shows the strategic value of a larger DC base. France, the UK, Italy and Spain demonstrate that larger markets are increasingly building more balanced networks.

For investors, CPOs and policymakers, the key question is shifting from “how many charge points are installed?” to “how well does the network perform?”

That means looking at uptime, utilisation, charging speed, grid readiness, site quality and customer experience. Scale still matters. But the structure and performance of that scale now matter just as much.